Why Merchant One is Best for Flexible Pricing

Merchant One provides credit card processing solutions for businesses of all sizes and adjusts its pricing based on factors, such as business size, industry and credit. We were impressed by the wide range of services, including entire POS systems with terminals and credit card readers that attach wirelessly to iOS or Android devices. We also like that Merchant One boasts a high approval rate and a quick turnaround of funds.

Merchant One, a reseller of Clover POS hardware, provides high-speed processing, supports gift and loyalty card programs and offers the ability to launch text message marketing campaigns. Its e-commerce offering has many more features, including a free shopping cart and remote access. Merchant One, which boasts a 98% approval rating, has 24/7 customer support and provides you with a dedicated account manager to help you throughout the setup process, which is not something all of those we researched offered.

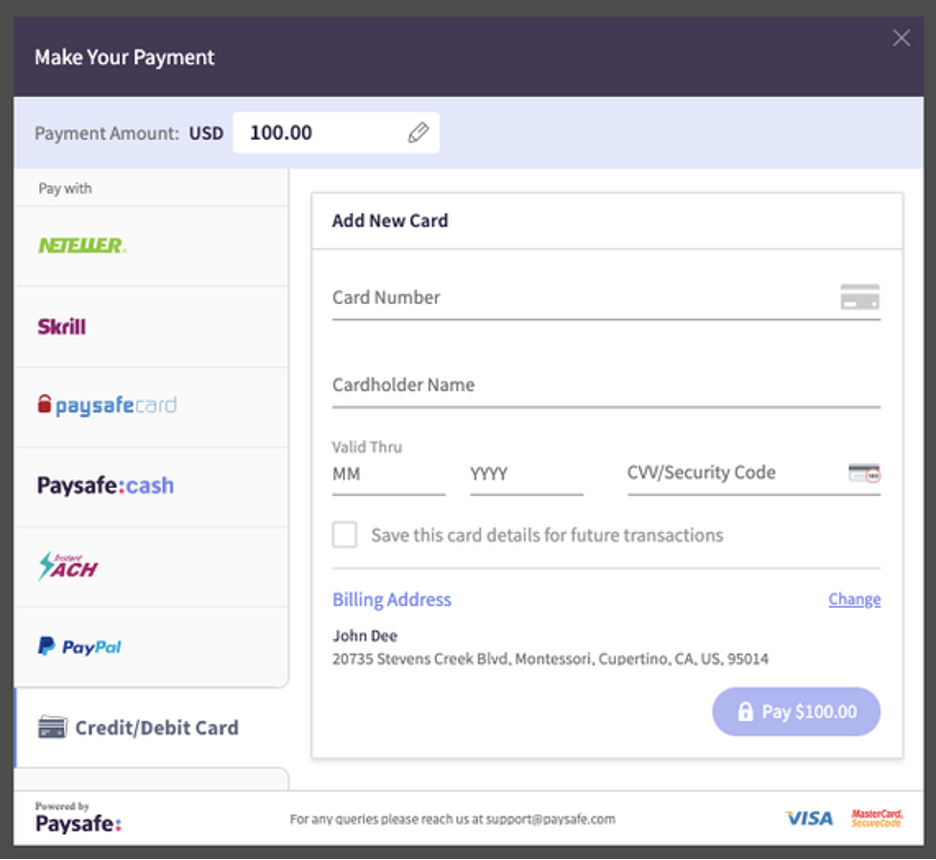

Merchant One features a sleek user interface. Source: Merchant One

Merchant One Costs

Monthly pricing

$6.95 a month, plus a $99 annual fee. Other monthly fees may apply.

Processing fees

Merchant One’s processing rates differ based on the exact type of business

- In-person transactions: 0.29% – 1.55%.

- Keyed-in transactions: 0.29% – 1.99%.

Hardware

Free hardware is available upon signup. Merchant One also resells Clover POS hardware.

Merchant One Advantages

- The pricing plans provide flexibility on rates, as well as free hardware.

- Merchant One’s subscription pricing is lower than many other processors.

- Merchant One receives excellent marks on TrustPilot for its customer service.

Merchant One Disadvantages

- Unlike other providers that we reviewed, Merchant One doesn’t manufacture its own hardware.

- Merchant One requires that you sign up for a three-year contract.

- An early termination fee may be assessed for each remaining month in your contract.

Merchant One User Scores

Trust Pilot: 4.8/5

“Gave genuine assistance, clarified information upon request, provided answers to all given questions and even enable us to receive discounts on our current rates. Great service. Much appreciated,” one user wrote.

Learn more about Merchant One in our complete review.