Gone are the days when businesses could get away with not accepting credit card payments. However, today, businesses need to do more than just accept credit cards, they need to be able to accept every payment type. This is why finding the right merchant services provider is critical for businesses. The best options not only allow you to accept a variety of payment types, but they also have transparent pricing, competitive rates and no lengthy contracts. With these factors in mind, we spent dozens of hours researching the top merchant account service providers and payment gateways to help you find the best options for your business. Check out our recommendations for the best merchant service providers for different business types below.

Business.com is supported by commissions from providers listed on our site. Read our Editorial Guidelines.

MENU

Starting a Business

Our Top Picks

Our In-Depth Reviews

Finance

Our Top Picks

Our In-Depth Reviews

Explore More

Human Resources

Our Top Picks

Our In-Depth Reviews

Explore More

Marketing and Sales

Our Top Picks

Our In-Depth Reviews

Technology

Our Top Picks

Our In-Depth Reviews

Business Basics

Our Top Picks

Our In-Depth Reviews

business.com

Advertising Disclosure

Advertising Disclosure

Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Updated Jun 26, 2024

The Best Merchant Account Services of 2024

Merchant account services like Merchant One will process your customers' credit card payments while assisting with PCI compliance.

Jennifer Dublino, Senior Writer & Expert on Business Operations

Editor Verified

Editor Verified

A business.com editor verified this analysis to ensure it meets our standards for accuracy, expertise and integrity.

Best for Flexible Pricing

Merchant One Merchant Services- Subscriptions $6.95/month

- Processing from 0.29%

- Free equipment

- Subscriptions $6.95/month

- Processing from 0.29%

- Free equipment

Best for POS

Clover Merchant Service- Subscriptions from $14.95/month

- Processing from 2.3% + 10 cents

- Equipment starting at $49

- Subscriptions from $14.95/month

- Processing from 2.3% + 10 cents

- Equipment starting at $49

Best for Startups

Square Merchant Services- Free version available

- Processing from 2.6% + 10 cents

- Free equipment

- Free version available

- Processing from 2.6% + 10 cents

- Free equipment

- Contact for a price quote

- Contact for a rate quote

- Free equipment

Best for Fast Setup

North American Bancard- Contact for a price quote

- Contact for a rate quote

- Equipment starting at $9.95/month

- Contact for a price quote

- Contact for a rate quote

- Equipment starting at $9.95/month

Table of Contents

At business.com, we’ve spent years advising entrepreneurs, creating actionable guides for obtaining funding and managing business finances, and comparing and contrasting leading software and services to identify the best financial tools for small and growing businesses. Our playbooks and explainers are packed with advice from real business lenders, accountants, credit card processing experts, tax advisers and other finance professionals.

To inform our financial software and service recommendations, we put ourselves in the shoes of business owners and test each product’s effectiveness while taking into account its cost. Every review, whether it be for a credit card processing solution or invoicing software, is infused with our guiding principles: accuracy and objectivity. Learn more about our editorial process.

How We Decided

To find the best merchant account services, we looked for payment processing vendors with transparent pricing, competitive rates, limited fees and fair contract terms. We considered how fast payments were processed, whether credit card readers were included or cost extra, and if the provider also offered POS and e-commerce tools. We also compared integration and customer service options across vendors.

102

evaluated

33

researched

6

chosen

To find the best merchant account services, we looked for payment processing vendors with transparent pricing, competitive rates, limited fees and fair contract terms. We considered how fast payments were processed, whether credit card readers were included or cost extra, and if the provider also offered POS and e-commerce tools. We also compared integration and customer service options across vendors.

102

evaluated

33

researched

6

chosen

Compare Our Best Picks

Merchant One Merchant Services | Clover Merchant Service | Square Merchant Services | Paysafe | North American Bancard | USBank | |

|---|---|---|---|---|---|---|

| Rating (Out of 10) | 8.5 | 8.8 | 8.4 | 8.5 | 8.1 | 8.4 |

| Best for | Flexible pricing | POS | Startups | Niche Businesses | Fast setup | Businesses on a Budget |

| Rate plans | Subscription plus flat rate | Subscription plus flat rate | Flat rate | Tiered | Interchange-plus, flat rate | Interchange-plus |

| Fees | Yes | Yes | No | No | Undisclosed | Varies |

| Contract length | 3 years | Month to month | Month to month | Month to Month | 3 years | Month to Month |

| Customer support | Yes | Yes | No | No | No | Yes |

| PCI compliance fee | No | Yes | No | No | Yes | No |

| Payout | Next business day | 1-3 days | 2-3 business days | Same day | Next business day | 2-3 business days |

| Early termination fee | Sometimes | No | No | No | Yes | No |

| Review Link |

Scroll Table

Our Reviews

- Base Price: Starting at $6.95 per month, plus a $99 annual membership fee.

- Top Features: Virtual terminal, reporting, e-commerce tools, 300 integrations, high approval rating, 24/7 support.

- Trial Period: There is no free trial currently available.

Why Merchant One is Best for Flexible Pricing

Merchant One, a reseller of Clover POS hardware, offers a comprehensive merchant account solution for businesses of all sizes. Merchant One’s pricing adapts to individual needs based on business size, industry, and credit history. With a high approval rate of 98%, we like that Merchant One accepts nearly all payment options and adjusts the pricing to reflect the risk profile. If your business becomes less risky by, for example, being in business for a longer period or raising its credit score, you can ask for a rate adjustment.

We were also impressed by their wide range of services, including complete POS systems with terminals and credit card readers and wireless options that connect to iOS or Android devices.

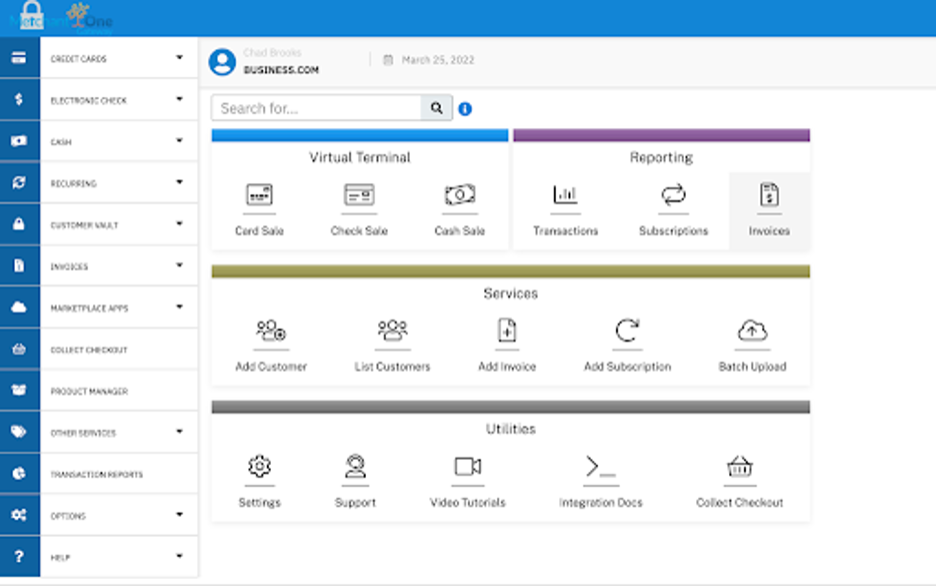

Merchant One’s user interface is easy to use and attractive. Source: Merchant One

Merchant One Costs

Monthly pricing

$6.95 a month, plus a $99 annual membership fee. Other monthly fees may apply.

Processing fees

- In-person transactions: 0.29% – 1.55%.

- Keyed-in transactions: 0.29% – 1.99%.

Hardware

Free POS hardware is available upon signup. Merchant One also resells Clover POS equipment.

Merchant One Advantages

- Merchant One offers flexible pricing plans with competitive rates and often includes free hardware, making it a budget-friendly option for many businesses.

- Compared to other processors, Merchant One’s subscription pricing can be more affordable, especially for businesses with predictable transaction volumes.

- Merchant One consistently receives high praise on platforms like TrustPilot for its exceptional customer service, ensuring you receive the support you need.

Merchant One Disadvantages

- As a reseller, Merchant One doesn’t manufacture its own hardware, potentially restricting your options and customization possibilities compared to providers with in-house hardware development.

- Merchant One requires a three-year contract, which might not be ideal for businesses seeking more flexibility or unsure about their long-term processing needs.

- Breaking the three-year contract incurs significant early termination fees, potentially making it difficult and expensive to switch providers if needed.

Merchant One User Scores

Trust Pilot: 4.8/5

“Very knowledgeable and friendly. Called me back to make sure everything was ok after she told me how to do a refund,” one user wrote.

Learn more about Merchant One in our complete review.

- Base Price: Starting at $14.95 for select entry-level plans.

- Top Features: Virtual terminal, inventory management, e-commerce tools, customer management, loyalty program, 500 integrations, reporting, proprietary hardware

- Trial Period: 90-day free trial for Clover’s software.

Why Clover is Best for POS Hardware

When it comes to merchant accounts with seamless POS integration, Clover shines thanks to its diverse hardware options. We were particularly impressed with the Flex, a handheld terminal perfect for processing transactions tableside. For businesses needing a complete POS system, the Clover Station offers a user-friendly experience. And for simple, on-the-go payments, the Clover Go reader pairs effortlessly with your smartphone, eliminating the hassle of accepting tap-and-pay transactions. We were even more excited to see that newer Go readers offer invoicing capabilities, expanding their functionality beyond basic payments.

We were also impressed with Clover’s customer management and marketing tools. With Clover, you can create and manage customer profiles and email them personalized offers based on their purchase history. You can solicit customer feedback via the app. When customers agree to receive their purchase receipts by text, they automatically opt in to text message marketing, giving you a highly effective customer engagement tool. The software also supports gift cards.

Clover offers a popular lineup of POS products. Source: Clover

Clover Costs

| Starter | Standard | Advanced | |

|---|---|---|---|

| Full-service dining | $150 | $195 | $290 |

| Quick-service dining | $90 | $130 | $175 |

| Retail shops | $60 | $130 | $175 |

| Professional services | $14.95 | $50 | $120 |

| Personal services | $50 | $90 | $130 |

| Home and field services | $14.95 | $49 | $50 |

Processing fees

| Card-Not-Present | Card-Present | |

| Starter | 5% + $0.10 | N/A |

| Standard | 5% + $0.10 | 2.6% + $0.10 |

| Advanced | 5% + $0.10 | 2.3% + $0.10 |

Hardware

- $49 mobile reader.

- $599 handheld terminal.

- $1,799 full-service register.

Clover Advantages

- Clover offers a variety of plans tailored to your business type, giving you the freedom to choose the perfect fit.

- Unlike some competitors, Clover’s subscription plans don’t charge extra per employee, keeping your costs predictable.

- Clover builds all their own POS hardware, so you can get everything you need in one place.

Clover Disadvantages

- While Clover’s pricing is flexible, high-volume businesses might find more cost-effective solutions elsewhere.

- Clover’s POS devices work best with their own processing system, which could limit your options if you prefer another provider.

- Unlike some competitors, Clover doesn’t offer a free trial of their software, making it harder to test before committing.

Clover User Scores

Trust Pilot: 3.6/5

“Clover POS is easy to use and has reasonable fees. I am glad I replaced another brand with Clover a few years ago,” one user wrote.

Learn more about Clover in our complete review.

- Base Price: Starting at $29 per month (free version is also available).

- Top Features: Virtual terminal, inventory management, SMS invoicing, reporting, e-commerce, 350 integrations, proprietary hardware.

- Trial Period: A 30-day free trial is available.

Editor's Rating: 8.4/10

Why Square is Best for Startups

As a merchant account provider, Square has impressed us with its accessibility and ease of use. Its free plan is ideal for low-volume businesses, allowing us to test their services risk-free. Additionally, the user-friendly interface makes it simple for anyone to start accepting credit cards quickly. We also appreciate the seamless integration with various business tools, streamlining operations and simplifying management. Finally, Square’s transparent pricing with clear fee breakdowns provides us with a clear understanding of our transaction costs. Overall, Square’s combination of affordability, ease of use, and powerful integrations makes it a strong contender for businesses seeking a reliable and user-friendly merchant account solution.

Square’s POS devices are well-known among small business owners for user-friendliness. Source: Square

Square Costs

Processing Rates

| Transaction Type | Fee |

|---|---|

| Swiped or inserted chip cards, contactless payments | 2.6% + $0.10 |

| Manually keyed-in payments, Card on File, Virtual Terminal | 3.5% + $0.15 |

| Invoices (Free plan) | 3.3% + $0.30 |

| Invoices (Plus plan) | 2.9% + $0.30 |

Hardware

- Free Square Reader for magstripe upon signup.

- $49 Square Reader for contactless and chip.

- $149 Square Stand for contactless and chip

- $299 Square Terminal

- $799 Square Register

Square Advantages

- Square’s user-friendly software and affordable POS hardware make it perfect for startups and businesses new to credit card processing. The accessible price point allows them to get started quickly and easily.

- Square lets you accept all major payment methods, including swipes, dips, contactless options, and even digital gift cards. This ensures you can cater to your customers’ diverse preferences.

- Square seamlessly integrates with popular e-commerce platforms and hundreds of business apps. This allows you to streamline your operations and manage your business more efficiently.

Square Disadvantages

- While Square avoids monthly subscription fees, its per-transaction fees can add up quickly, especially for businesses with high transaction volume.

- Square offers a variety of POS hardware options, but none are available for free.

- Square’s free invoicing plan has limitations in terms of features and functionality. Upgrading to their Plus plan with advanced invoicing capabilities comes with an additional monthly fee.

Square User Scores

Trustpilot: 4.0/5

“Allows you to communicate, take payments as well as advertise your business. The low fees to transfer money between the website and your business banking is also a plus,” one user wrote.

Learn more about Square in our complete review.

- Base Price: Contact the company for a custom quote.

- Top Features: Next-day funding, iAccess business portal, solutions for employee and inventory management.

- Trial Period: There is no free trial, but a demo is available for potential customers.

Why Paysafe is Best for Niche Businesses

Paysafe sets itself apart by catering to specific industries with specialized solutions. It offers tailored merchant account services for businesses in retail, hospitality, convenience stores, gas stations and direct marketing. But, we especially like its willingness to work with businesses in often-excluded industries like cryptocurrency, video gaming and forex, offering them access to reliable and secure payment processing. We think that flexibility and industry expertise make Paysafe a valuable option for businesses seeking a merchant account provider that understands their unique needs.

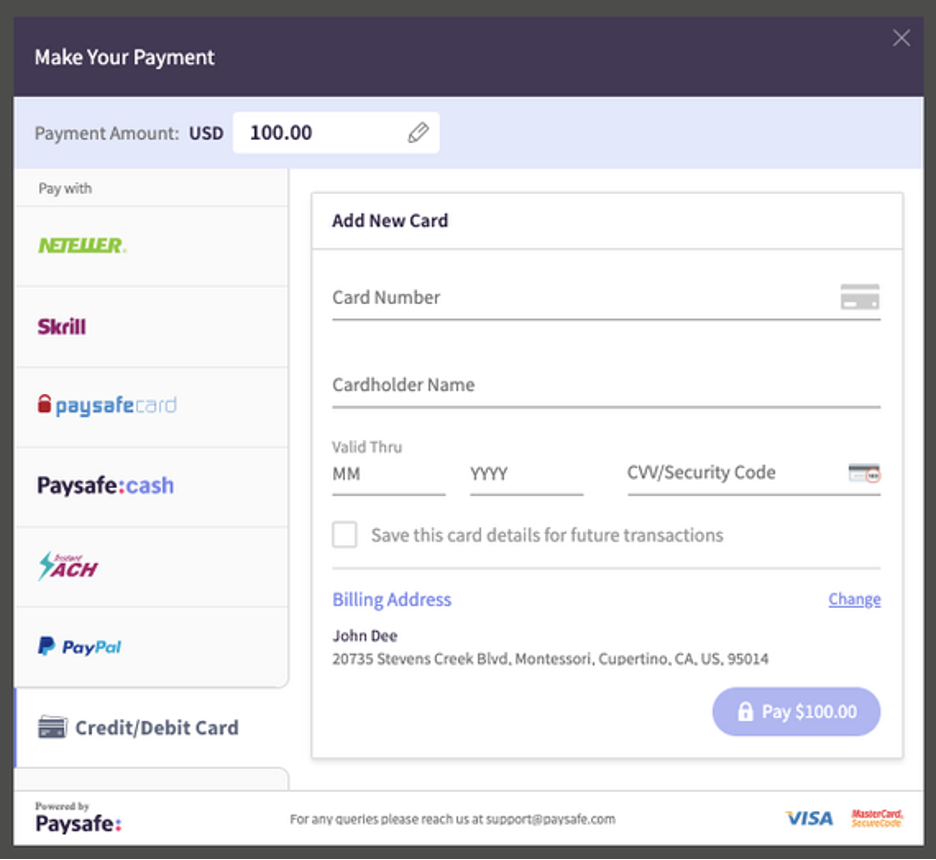

Paysafe offers a secure e-commerce checkout form, among other tools. Source: Paysafe

Paysafe Costs

Paysafe uses a quote-based pricing model, meaning they provide customized rates based on your business needs. Contact them for a personalized quote.

Paysafe Advantages

- Paysafe’s quote-based pricing model allows for negotiation, potentially leading to lower rates than the standard interchange-plus model offered by some competitors, especially for high-volume businesses.

- Paysafe goes beyond basic processing by catering to specific industries, such as convenience stores, digital marketing, and even regulated online gambling. This focus allows them to offer tailored features and compliance expertise relevant to your unique business needs.

- If you already use Paysafe’s prepaid cards or digital wallets, you can easily integrate credit card processing for a unified payment system, streamlining your operations and providing a consistent customer experience.

Paysafe Disadvantages

- Compared to competitors with clear fee breakdowns, Paysafe’s quote-based pricing and lack of readily available pricing information online can make it difficult to assess overall costs and compare them to other options.

- Setting up and using Paysafe might require more effort compared to user-friendly options like Square or Stripe, potentially leading to a steeper learning curve and increased setup time.

- Finding clear and accessible pricing details on Paysafe’s website can be challenging, requiring you to contact them directly for a quote, which can be inconvenient and time-consuming.

- Base Price: Contact the company for a quote.

- Top Features: Reporting, virtual terminal, e-commerce, inventory management, cash discounting program.

- Trial Period: There is no free trial currently available.

Editor's Rating: 8.1/10

Why North American Bancard is Best for Fast Setup

North American Bancard stands out for its streamlined approach to merchant accounts. We appreciated the smooth application process with quick approvals, making it easier for businesses to get started quickly. Additionally, they are willing to work with businesses in high-risk industries, expanding their accessibility. We like that North American Bancard also provides free equipment and offers next-day funding for deposited funds, improving businesses’ cash flow.

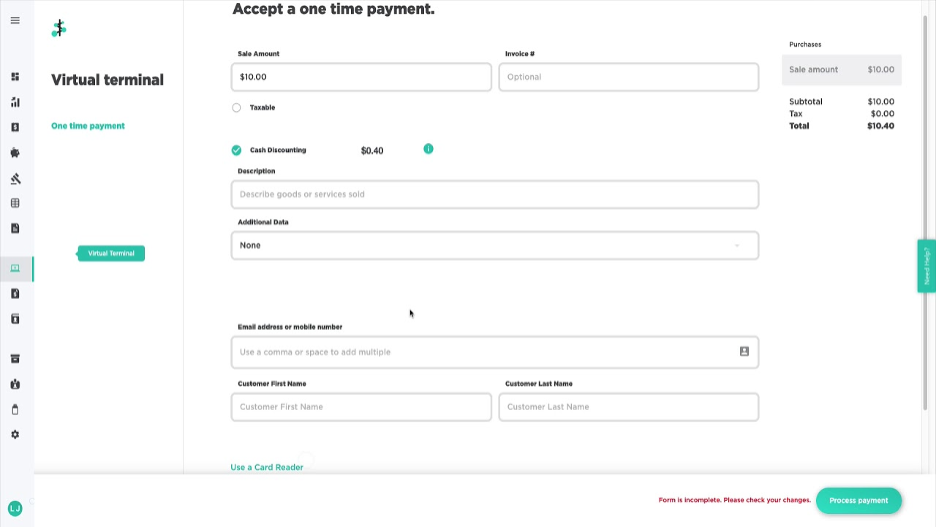

Payments Hub’s virtual terminal allows you to manually input transactions. Source: North American Bancard

North American Bancard Costs

While North American Bancard doesn’t publicly disclose its specific rates, its pricing is tailored to individual businesses and takes factors like size and transaction volume into account. To get an accurate quote for your specific needs, contact them directly for a personalized consultation.

North American Bancard Advantages

- North American Bancard stands out for its willingness to work with businesses in high-risk industries, making it a valuable option for those often excluded by other providers.

- Their unique EDGE program offers customers a cash discount incentive, potentially reducing processing fees for businesses that primarily deal in cash transactions.

- North American Bancard boasts a quick and easy application process, complete with free equipment, making it a convenient choice for businesses seeking a smooth onboarding experience.

North American Bancard Disadvantages

- Unlike some competitors, North American Bancard doesn’t publicly disclose its processing rates, requiring you to contact them directly for a personalized quote.

- Feature Gap: While North American Bancard offers a solid core service, their offering may lack some of the advanced features and integrations provided by competitors.

- Potential Hidden Fees: Be aware of potential termination fees and other charges that might not be explicitly mentioned upfront.

Learn more about North American Bancard in our complete review.

- Base Price: Starting at $15 per month (a free version is also available).

- Top Features: Free POS hardware rentals, same-day funding, integrated Talech POS system, merchant services, Buy Now, Pay Later, EMV chip card processing

- Trial Period: There is no free trial currently available.

Editor's Rating: 8.4/10

Why USBank is Best for Businesses on a Budget

We were impressed with USBank’s merchant account services, particularly for budget-conscious businesses. Its free rentals of essential POS hardware make it easy to get started without a large upfront investment. Additionally, the tiered pricing structure is clear and transparent, so there are no hidden fees to worry about. We were also particularly impressed with the same-day funding feature, which helps businesses access their processed transactions faster than some competitors, keeping cash flow smooth. Overall, USBank strikes a perfect balance between affordability and functionality, making them a great choice for businesses on a budget.

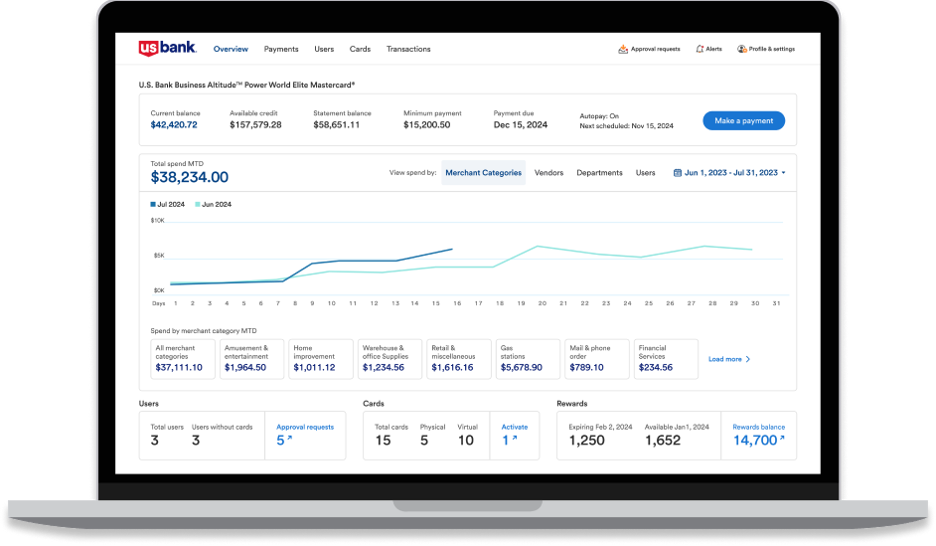

USBank’s useful dashboard provides an overview of your business. Source: USBank

USBank Costs

Processing Rates

| Transaction Type | Fee |

|---|---|

| Swipe, tap, insert | 2.6% + $0.10 |

| Keyed-in transaction | 3.5% + $0.15 |

| Online transactions | 2.9% + $0.30 |

Hardware

USBank offers flexibility in its merchant account setup. You can choose from free hardware rentals or opt for a paid monthly plan that includes POS equipment. These plans range from $15 to $99 per month, allowing you to find the option that best suits your budget and merchant account needs.

USBank Advantages

- USBank offers competitive rates on their starter merchant account plans, making them a budget-friendly option for businesses getting started. Some plans even include free rentals of basic POS hardware, further reducing the initial investment.

- Unlike some competitors, US Bank stands out with features like same-day funding for processed transactions. This allows businesses to access their funds quickly, improving cash flow and financial flexibility.

- USBank offers bundled solutions with Talech POS systems, which can be conveniently combined with their processing services. This provides a one-stop shop for businesses seeking both hardware and processing solutions.

USBank Disadvantages

- While USBank offers tiered plans, their structure might be less transparent than competitors who use a clear interchange-plus breakdown.

- While the bundled solution with Talech POS is convenient, the overall user experience might depend heavily on the specific POS system you choose.

- Compared to widely used processors, finding user reviews and feedback for USBank’s merchant account services might be more challenging.

Additional Options Worth Exploring

Helcim

We are impressed that Helcim goes above and beyond with its comprehensive software, offering features like POS services, customer management, inventory management, and employee tracking. These capabilities, often reserved for higher-tier plans with other providers, make Helcim a versatile platform for businesses seeking a complete solution.

Sekure

Sekure operates as a merchant account broker, giving you the power to choose from multiple payment methods and tailor a plan that aligns perfectly with your budget and transaction volume. We appreciate Sekure’s guidance in navigating the merchant account landscape and finding a reliable provider that delivers personalized service.

Chase Payment Solutions

As a major bank and credit card issuer, we like that Chase boasts unparalleled insight into consumer spending habits. Businesses utilizing Chase Payment Solutions can leverage this vast data trove to effectively target potential customers. With this data, you can gain insights into demographics, spending patterns, and purchasing behavior to reach the right customers with the right message.This unique feature sets Chase apart and makes them our pick for businesses seeking data-driven insights.

Stripe

Online businesses will love Stripe’s user-friendly platform and seamless integration with popular e-commerce platforms like Shopify and Magento. Setting up online payments is a breeze, and the ability to customize our store and utilize robust security features makes Stripe a compelling choice. We like that you can easily connect Stripe with your existing e-commerce platform for a smooth checkout experience for your customers.

National Processing

National Processing stands out with its competitive interchange-plus rates and a rate-lock guarantee, ensuring our rates won’t increase during the contract. They also offer to match or beat competitor rates, demonstrating their commitment to affordability. We like that you can lock in your rates at the time of signup, providing peace of mind and predictability for your budgeting.

Flagship Merchant Services

Flagship Merchant Services offers month-to-month contracts with no cancellation fees, making them our pick for flexibility. This allows you to easily adjust your merchant account services as your business needs evolve. We appreciate that you can avoid long-term commitments and enjoy the freedom to adjust your services as needed without penalty. You can also exit your contract at any time without incurring additional charges, providing peace of mind and flexibility.

Finix

Finix is a game-changer for businesses experiencing rapid growth. Unlike one-size-fits-all solutions, Finix allows you to completely customize the payment experience. We love that you can build a system that perfectly aligns with our unique needs and seamlessly integrate it with existing tools. Finix is built to handle our growth and adapt alongside expanding business, allowing you to add new features and expand your payment capabilities as your business scales.

Finix’s open API allows you to build custom integrations. Source: Finix

Pricing

Cost is often a top factor when you’re looking for the right merchant account services for your business. If you process a lot of card payments each month, it can be expensive if you go with the wrong provider. There are three types of costs you need to investigate:

- Processing fees

- Account fees

- Equipment costs

Many of the best merchant services and payment gateway providers post pricing on their websites. However, more commonly, you’ll have to speak with a sales representative. During these calls, the rep will ask about the specifics of your business, such as your transaction volume, average ticket size, industry and creditworthiness. If you’re already processing, many reps will ask you to send them a recent statement so they can try to meet or beat your current rates.

Processing Fees

Whether you accept credit card payments online or in person, you pay a small fee for every transaction, which is expressed as a percentage of the sale plus a few cents. However, providers calculate these costs differently, which makes it difficult to compare prices. To make an accurate comparison, you need to know the types of processing fees and pricing models.

Processing fees have three parts: the interchange rate, the card-brand fee and the processor’s markup.

- The interchange rate: This is a non-negotiable cost set by the card brands (American Express, Discover, Mastercard and Visa), and every service provider pays the same amount. Each card brand has its own rate table with different interchange rates based on the type of card (credit or debit, regular or rewards, etc.), your industry, the size of the sales ticket and how the card is accepted (in person or online, using a chip card reader or swiper, etc.).

- The card-brand fee: This is also a non-negotiable fee that the card networks charge; every processing service provider pays the same amount.

- The processor’s markup: This portion of the fee is negotiable.

Recognizing how confusing this is, many processors try to simplify processing rates and how they communicate them to their merchants. Most use one or more of these three pricing models: interchange-plus pricing, tiered pricing and flat-rate pricing.

Interchange-plus pricing: Industry experts favor this pricing model – sometimes called interchange pass-through pricing or cost-plus pricing – because it’s the only pricing model that shows you exactly what the processor’s markup is. This is significant because the markup is the only part of the cost that you can negotiate. As a result, this model has the best pricing for most merchants.

- When you’re quoted this rate, it will look something like this: 0.3% plus $0.15. Remember, this is only the processor’s markup; you still must pay the interchange and assessment fees. For example, if you have a retail business and you accept a rewards Visa card in person using a chip card reader, the interchange fees might be 1.65% plus $0.10. The card association fee for Visa would be an additional 0.15% plus $0.02. Adding up all three costs, the full rate you would pay for this transaction would be 2.1% plus $0.27.

Tiered pricing: Though this is the most common pricing model, industry experts criticize its lack of transparency. Other names for this model include bundled pricing and bucket pricing, because it attempts to bundle interchange fees, card-brand fees and markups, and then segment transactions into tiers, or buckets. These tiers are often sorted into qualified, midqualified and nonqualified, with separate tiers for debit and credit card transactions.

The low teaser rates that many companies advertise are usually qualified debit transactions, which means they apply only to regular debit cards that you accept in person using a card reader. Midqualified transactions are usually rewards cards, and nonqualified transactions are most often business or foreign cards, though some also include premium rewards cards. Most merchant service providers offer three tiers, but some have as few as two or as many as six.

- When you see this rate advertised, it looks something like this: 1.39% plus $0.21. However, this rate is only for debit cards accepted in person, so if you accept a credit card, you’ll pay a different rate, perhaps 1.59% plus $0.21. If it’s a rewards card, it would be downgraded from qualified to midqualified, which might add another 1% to the cost. So, for this example, the rate would be 2.59% plus $0.21.

If you’re quoted tiered rates, it’s important to ask how many tiers there are and which types of cards and acceptance methods apply to each. Make sure you know which types of cards your customers use most so you can judge whether this pricing model is cost-effective for your business. If the majority of your customers use regular debit cards and you accept cards in person, this processing model may be worth considering; otherwise, you should look for a processor that offers one of the other pricing models.

Tip

If you go with a tiered pricing plan, find out how many tiers there are and which types of cards and payment methods apply to each tier.

Flat-rate pricing: Most of the merchant services companies that use this simple pricing model charge a single fixed percentage rate per transaction, though some also charge a per-transaction fee. This pricing model is popular with mobile merchant service providers, and it may be the most cost-effective option for small businesses that process less than $3,000 per month or have small tickets. This type of transaction rate is noticeably higher than those from the other two pricing models, but there usually are no other account fees; all you pay are the processing fees for each transaction, which is why it’s such an attractive option for new and very small businesses.

- When you see this rate advertised, it looks something like this: 75%. Using the above scenario with the rewards credit card, this is the processing fee you would pay. It is higher than the other two pricing models’ fee percentages, but there aren’t any other fees for your account, which may make it less expensive overall, depending on how much you process each month and which types of cards your customers prefer. The consistent rate makes it easy for you to calculate exactly how much you’ll pay in processing fees each month.

Merchant Account Fees

In addition to the processing rates for each transaction, you’ll pay account maintenance fees if you’re working with a full-service merchant account provider or payment gateway service. These typically use the interchange-plus or tiered pricing models. Generally, providers that use the flat-rate processing model don’t charge account maintenance fees.

When you ask about account fees, most sales reps will tell you about the monthly fee, but there are a lot of complaints online about surprise fees on credit card processing statements. For this reason, it’s important to read the full contract (application, terms of service and program guide) to ensure you’re aware of every fee.

Here are some of the fees most merchant services providers charge. For a detailed list of fees to look for as you read processing contracts, see our guide to credit card processing fees.

- Monthly fee: Most merchant service companies charge a monthly fee, sometimes called a statement fee, that covers the cost of preparing your monthly billing statement and providing customer support. This fee usually ranges from $5 to $15. Some providers may charge more if they roll other regular account fees into this charge.

- Gateway fee: A payment gateway is necessary if you intend to accept credit cards online. Small business owners with an online shop need a gateway because it encrypts and securely transmits credit card data from your website to the processor. Pricing varies; some processors charge a monthly fee of around $10 for this service, some charge a per-transaction fee ranging from $0.10 to $0.25, and some charge both.

- PCI compliance fee: If you work with a standard processor that gives you your own merchant account, you’re required to be PCI-compliant. That designation means you adhere to the Payment Card Industry (PCI) Data Security Standard, which was developed to help merchants prevent data theft and fraud. Most processors that charge this fee offer to help you complete the annual questionnaire that is required to demonstrate your compliance. Your rep may call or email to remind you to take the assessment each year, or the processor may note it on your statement. On average, this fee is $99 annually.

- PCI noncompliance fee: Even if the processor doesn’t require you to pay an annual PCI compliance fee, it may charge you a monthly noncompliance fee if you fail to establish compliance by filling out the annual questionnaire. You can easily avoid this fee by staying up to date with your PCI responsibilities. This fee can be very high, ranging from $20 to $60 per month, as it is meant to discourage you from letting your PCI compliance lapse.

- Chargeback fee: If a customer disputes a charge and requests their money back, the processor charges you this fee. Chargeback fees are usually $15 to $25. Chargebacks are more common when you accept credit cards online versus in person, because typical reasons for chargebacks include delivery failures, technical errors, fraud and customer dissatisfaction. Another common cause of chargebacks is if your store name is different from the name on your merchant account and your customer doesn’t recognize your merchant name on their credit card statement.

Some processors charge application and setup fees for your merchant account, a payment gateway setup fee to connect the payment gateway with your website, and an early termination fee if you want to close your account before the contract’s term expires. The best providers don’t charge these fees, though, so you should ask them to waive these fees if they’re included in your quote or look for a provider that doesn’t tack them on.

Tip

Avoid merchant account providers that charge an application or setup fee. The best providers won’t hit you with these extra expenses.

Processing Equipment Costs

If you accept credit cards in person, you need to purchase a card reader or terminal. Here are the three most popular options:

- Mobile card readers: This is the cheapest option, as many providers give you a free swiper when you sign up for an account. If you want to purchase a mobile card reader that also accepts EMV chip cards, contactless cards and mobile payments, these cost less than $100.

- Credit card terminals: This is the midrange option. These devices cost $150 to $600, depending on whether you choose a countertop or wireless unit. They have built-in keypads and receipt printers, and all new models can accept both chip cards and contactless payments.

- POS systems: This may be the most expensive option, but cost will depend on the type of system you choose. Tablet POS systems are often the least expensive, and they work with mobile card readers.

The most important thing to know about processing hardware is to avoid leasing it, because you can’t cancel a leasing contract and, in most cases, you’ll pay much more over the long term than if you purchase it outright. It’s enough of a problem that the Federal Trade Commission cautions against it, noting that businesses that lease may pay thousands of dollars for equipment that costs just a few hundred dollars.

Many businesses require POS equipment to process credit cards. Source: Clover

Features

Whether you work with a merchant services provider, a payment gateway provider or a credit card processing company that provides you with both a merchant account and a payment gateway, the company you choose should be up to date with industry standards and allow you to accept all major cards (American Express, Discover, Mastercard and Visa). Here are more qualities you should consider as you look for a merchant processor for your small business:

- Pricing: The best service providers are transparent about pricing, either by clearly posting their rates, fees and processing hardware costs on their websites, or by making it easy to get a quote from a company representative. Look for a merchant account service that offers interchange-plus pricing and doesn’t charge setup fees, cancellation fees or nonstandard fees, like quarterly technology fees or semiannual postage and handling fees.

- Contracts: Choose a service provider that offers month-to-month or pay-as-you-go terms so you can cancel without penalty if you find a better deal elsewhere. Standard payment processing contracts have three-year terms and charge hefty early termination fees; some even have liquidated damages clauses.

- Scalability: As your business expands, you may want to accept credit cards online in addition to in-store and on the go, so look for a company that offers multiple ways to accept payments. You should also be able to add registers, or even locations, to your account.

- Security: The credit card processing company providing your payment gateway and merchant account should comply with the PCI Data Security Standard. It should also help you become PCI-compliant.

- Processing hardware: The services provider should offer card readers or terminals that are EMV- and NFC-capable so you can securely accept chip cards, contactless cards and mobile payments such as Apple Pay and Google Pay. It should also allow you to purchase the hardware upfront so you can avoid bad leasing contracts and the headaches that come with them.

Square offers some inexpensive processing tools, including this mobile reader. Source: Square.

- Integrations: If you have a website or use other business software – such as an e-commerce platform, a top POS system, highly rated customer relationship management software or accounting software – you’ll want a merchant account or payment gateway that integrates with those platforms so you can easily sync data instead of manually downloading and uploading it between systems.

- Payouts: It’s important to consider how and when you receive your money after a sale. Most service providers offer next-day funding, taking one or two days to deposit your money into your business bank account, and some can do it even faster, offering same-day or instant funding for a fee. Some providers give you the option of having your money loaded onto a business debit card.

- Customer support: The company’s customer service team should be readily accessible. The best providers offer 24/7 customer service so you can resolve issues no matter when you call.

- Other benefits or service limitations: If there are certain features you need – for example, a virtual terminal so you can accept payments using a computer with internet access – make sure to look for them before selecting a processor. Also consider whether there are certain limitations, such as monthly processing limits or vendors that support only one acceptance method.

Payment Processing Contracts

The best merchant account contracts have month-to-month terms with no early termination fees. However, the standard merchant account contract has a three-year term that automatically renews for an additional one or two years. If the processing service provider you want to work with has a lengthy contract, ask the sales rep if they can give you month-to-month terms. They want your business, and many are willing to negotiate.

With a standard merchant account contract, you have a very short window at the end of the term, usually 30 days, in which to cancel your account without penalty if you don’t wish to renew. Most providers require you to submit a cancellation request in writing.

If you miss this window or decide to close your account early, the company may charge you an early termination fee, which is usually a few hundred dollars. Some contracts also have liquidated damages clauses, which can make it very expensive to get out of your contract.

No matter which service provider you choose, it’s important to read the entire contract (the application, the terms of service and the program guide) before you sign anything or give the company your bank account information and Social Security number. Be aware of all the fees listed in the contract, as you will be expected to pay them even if they weren’t disclosed by a sales rep. If the sales rep offers to reduce or waive the term length or certain fees, get that in writing by amending the contract or receiving a written waiver.

Tip

Avoid merchant account providers that try to lock you into a long-term contract. Most of our best picks charge you on a month-to-month basis.

Frequently Asked Questions About Merchant Services

A merchant account is a type of bank account that allows you to accept payments from your customers using credit and debit cards. The credit card processing company sets it up for you and assigns you a merchant ID number. Once you start accepting credit card payments, the company holds your funds until settlement, when they are transferred to your business bank account.

If you sign up for a processing account with a payment facilitator (PayFac) or aggregator like Square or PayPal, you don’t need your own merchant account. Instead, you sign up as a submerchant under the provider’s master merchant account.

The benefit of working with a PayFac is that it’s faster and easier to set up your account, service is provided on a pay-as-you-go basis, and there are usually no account maintenance fees. But there are some limitations. Most aggregators don’t work with high-risk merchants, so if your business is in a high-risk industry, you’ll need to get your own merchant account. PayFacs are also more risk-averse than full-service payment processors, which means that your funds could be held if something about a transaction raises a red flag.

There are also some advantages of having your own merchant account. You can often get lower rates and better customer service, and the likelihood of having your money held or your account frozen is lower. There are account maintenance fees, but if your processing volume is high enough, they’re offset by the lower transaction rates.

A payment gateway is the technology that creates a secure connection between your website or browser and the credit card processing company, encrypting payment data for each credit card transaction. Some merchant services companies have proprietary payment gateways, but most set you up with a third-party payment gateway, such as those from Authorize.net and NMI.

The advantage of setting up a payment gateway through your merchant account provider is that it reduces the likelihood of compatibility issues and, in some cases, can be less expensive. For instance, you may not be required to pay a gateway setup fee if you go through your service provider instead of going direct. Also, depending on your processing contract, there may be an exclusivity clause that requires you to go through your merchant account provider.

Each time you run a transaction online or a customer makes a purchase on your website, the credit card information enters the payment gateway, where it’s encrypted and routed through a secure connection to the credit card processor, the card network, the bank that issued the card and your business’s bank account. Your customer’s card is charged for the transaction amount, and you receive the funds from the sale, minus the processing costs.

It depends. If you want to accept credit cards online and in person, you will need both a merchant account and a payment gateway. If you accept credit and debit cards exclusively using a credit card terminal, you won’t need a payment gateway. But you will need one if you use your computer as a virtual terminal or accept cards through your website.

When signing up for a merchant account, you should have several things on hand to make the process move smoothly. Most credit card processing companies require some general information on your business so they can determine whether you are a high or low risk.

A business’s risk level depends on factors such as its potential to be a victim of credit card fraud or experience a high rate of returns. Payment processors also consider how long a business has been in operation, since they are reluctant to lend money to what may amount to a fly-by-night operation. [Related article: Credit Card Processing in High-Risk Industries]

Most payment processors also want information on the business’s history, including any bankruptcies, defaults or previous merchant accounts on its record. In addition, most processors want information on the business owner, including their personal credit history, as many contracts require the business owner to sign a personal guarantee.

Some merchant account providers charge application and setup fees, but this is unusual among the best processors. You may want to consider other options if the company charges these fees.

Few things in this world are free, so avoiding merchant fees altogether isn’t realistic. That being said, there are ways to limit your costs. A good opportunity to do so is by looking for a service that offers a subscription pricing model. This ensures your interchange rates don’t fluctuate, and it may remove some of the added fees.

What to Expect in 2024

We expect businesses, especially small businesses, to pay close attention to the fees merchant services providers are charging them. Over the last few years, the use of digital payments has increased dramatically. The use of cash was already declining, but the pandemic accelerated this process. Today, approximately 60 percent of consumer transactions are made using credit or debit cards. This underscores the importance of credit card processing and associated services, including merchant accounts.

Visa and Mastercard increased interchange fees after several years of pandemic-induced delays. Large merchants are impacted most by these fee increases, although some small businesses with low volume or small transactions may actually see lower fees. Visa and Mastercard are planning to raise these fees again in 2024.

Improving the customer experience will continue to be a priority in 2024 for those in the payment industry. Giving consumers the ability to pay when, where and how they want will be merchant services providers’ focus in the coming year. The pandemic has shown that consumers now want many options regarding how and when they pay for goods and services. It will be up to those in the payment industry to deliver these choices.

“It’s not enough anymore to just offer payment solutions that are tailored to consumers; now, payments need to be taken right to them,” said Michel Léger, executive vice president of global sales and marketing at Ingenico, in a statement.

An Ekata survey of more than 7,000 consumers throughout North America and Europe revealed that 92% expect a secure, fast and frictionless payment experience, while more than 70% believe that online shopping account creation should be instantaneous.

To support those desires, mobile payments will continue to be paramount for merchant services providers. Finding better ways to support mobile shopping, mobile wallets and mobile checkouts will be a top priority for payment providers this year.

Data security and fraud prevention will remain a top concern for the payments industry over the coming years. According to the Ekata report, over 60% of consumers feel that businesses accessing their personal data are responsible for fraud prevention. Small businesses are benefiting from the strides made in artificial intelligence (AI) to bolster their security measures. Merchant accounts now utilize AI algorithms to analyze transaction data, recognize patterns, and swiftly identify potential fraudulent activities in real time.

In addition to accepting mobile payments, you should focus on finding ways to let your customers pay with mobile wallets and contactless cards that use near-field communication (NFC) technology in 2024. This technology has grown rapidly in popularity, and we expect it to continue.

Jennifer Dublino, Senior Writer & Expert on Business Operations

Jennifer Dublino is an experienced entrepreneur and astute marketing strategist. With over three decades of industry experience, she has been a guiding force for many businesses, offering invaluable expertise in market research, strategic planning, budget allocation, lead generation and beyond. Earlier in her career, Dublino established, nurtured and successfully sold her own marketing firm.

Dublino, who has a bachelor's degree in business administration and an MBA in marketing and finance, also served as the chief operating officer of the Scent Marketing Institute, showcasing her ability to navigate diverse sectors within the marketing landscape. Over the years, Dublino has amassed a comprehensive understanding of business operations across a wide array of areas, ranging from credit card processing to compensation management. Her insights and expertise have earned her recognition, with her contributions quoted in reputable publications such as Reuters, Adweek, AdAge and others.